The origins and scale of hedge funds

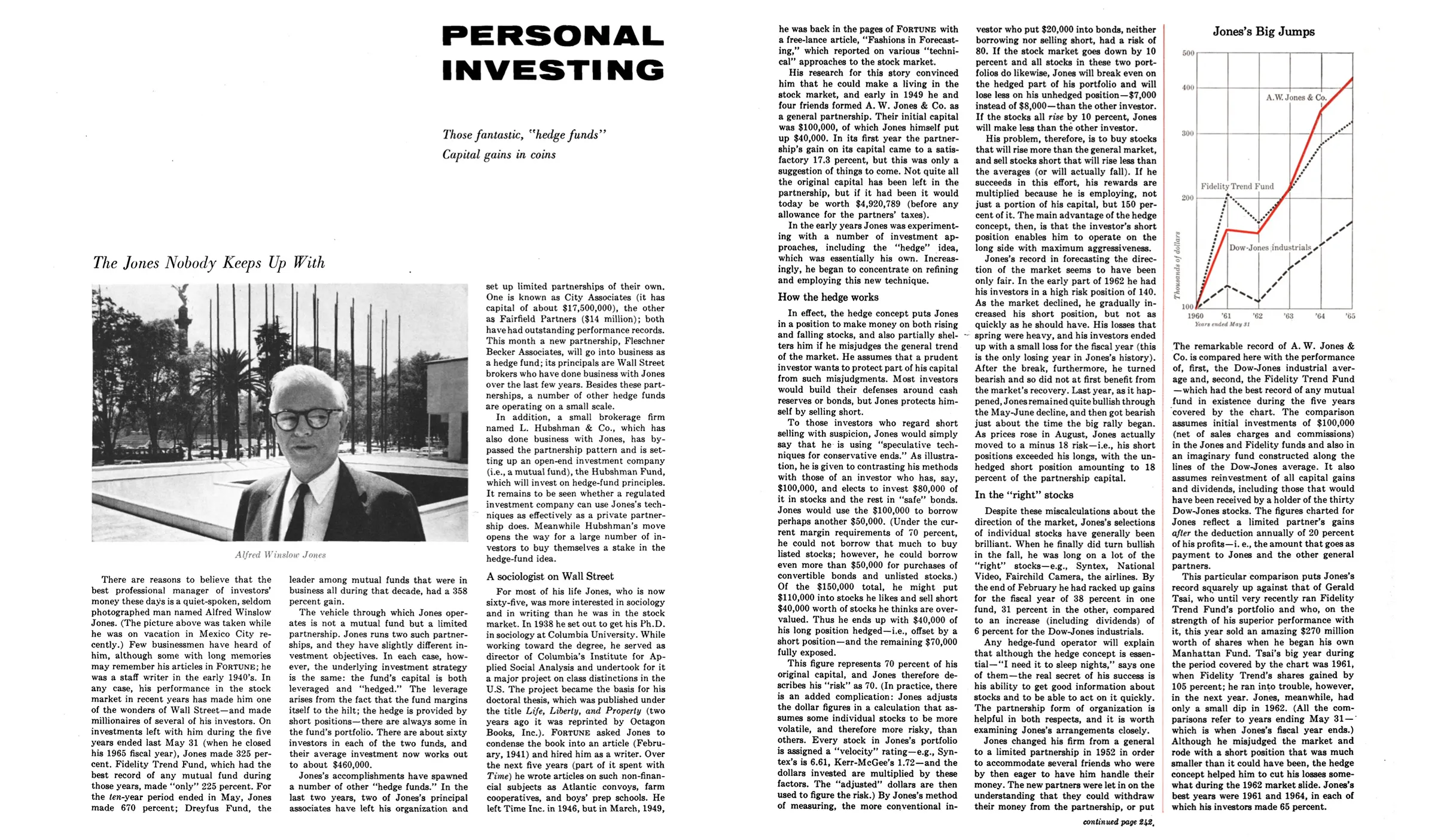

The first hedge fund is usually credited to Alfred Winslow Jones, a Harvard graduate who launched his fund in 1949.

Jones ran it as a general partnership, which kept him clear of the rules that bound mutual funds. In 1952, he reorganized it as a limited partnership and began taking a fifth of the profits. He borrowed to buy some shares and sold others short to soften market swings. That long/short approach to hedging the risk is where the name comes from. It caught on after Carol Loomis profiled him in Fortune in 1966. By the end of the 1960s, others, including Michael Steinhardt and George Soros, had launched their own funds.

Today, there is still no statutory definition of a hedge fund. In practice, the term means a private, actively managed fund sold only to wealthy investors. Because it is sold privately, it skips most of the rules that limit retail funds. The following features stand out:

- Open-ended. Investors can usually subscribe and redeem on a set schedule, not a closed-end fund with a fixed term.

- Liquid instruments. Invests in liquid assets: listed securities, bonds, indices, commodities, and increasingly cryptocurrencies.

- Flexible and higher-risk. Far more flexible, and higher-risk, than mutual funds.

- Leverage. Often borrows money (leverage) to boost returns.

- Two-part fees. Charges a management fee (1–2%) and a performance fee (commonly 15–20%).

- Wealthy investors only. Offered only to wealthy investors; offshore vehicles typically require at least $100,000.

- Regulated on three fronts. Managing the assets, the fund vehicle itself, and offering interests to investors are each regulated, often separately across countries.

They also differ sharply from mutual, venture, and private-equity funds, not just in risk and return, but in how they are built, who can invest, and how investors get their money back.

| Dimension | Hedge fund | Mutual fund | Venture capital | Private equity |

|---|---|---|---|---|

| Open vs. closed | Open-ended | Open-ended | Closed-end, ~8–13 yr life | Mostly closed-end; evergreen growing (~5% of PE assets) |

| Commitments | Subscribe on entry | Subscribe on entry | Subscribe on entry, drawn as called | Commitments drawn over time |

| Investments | Liquid: stocks, bonds, indices, commodities, crypto | Treasuries / index funds; leverage & shorting restricted | Illiquid early-stage equity or future-token rights | Control stakes in mature companies |

| Admission | Any time, accredited | Any time, no capital requirement | At launch, accredited; later entry rare | At launch, accredited |

| Redemptions | Redeemable with prior notice | Free entry/exit | No exit before term; fee + approval | No exit before term |

| Management fee | % of net asset value (NAV), marked continuously | % of assets under management (AUM) | % of AUM | % of committed, then invested, capital |

| Performance fee | % of NAV growth, annual | None | Carried interest (~20/80) | Carried interest |

| Strategy | Active trading, often levered | Liquid, lower-risk, lower return | Invests early then follows on | Invests to create value & exit at a premium |

Across all these vehicles, hedge funds have grown fast: the industry has roughly quadrupled since the 2008 crisis, passing $6 trillion in 2025.

Fund structures

For all the aura of mystique and complexity around hedge funds and the industry, every one is the same handful of parties, tied together by a few contracts and legal entities. Start with the plain-vanilla version below. Tap or hover over any box to see what it is and why it sits there.

There are two standard set-ups: with a separate general-partner entity, and without one (toggle above). In the combined version, a single management company is both the general partner, which puts up the GP commitment and takes the carried interest, and the investment manager, which runs the portfolio for the management fee. Splitting the general partner into its own entity ring-fences that liability and keeps the carry cleanly apart from the fee for tax purposes, which is why larger managers often prefer it.

The base structure above then branches into several more involved set-ups. What drives the choice is almost always tax: the tax status of the key limited partners, how the fund’s portfolio investments are taxed, and where each party is resident for tax (for example, whether the holdings are U.S. securities or foreign ones). Because a large share of the capital usually comes from U.S. investors, the structure a fund adopts is mostly driven by whether U.S. investors sit among its limited partners. That leads to the structures below.

Having mapped the key legal fund structures, let’s turn from how a fund is built to how it is regulated. Regulation falls into three layers: the manager, the fund itself, and the offering of its interests to investors. Each is the subject of one of the next three sections.

Regulating the management company

Managing a fund’s assets is a regulated activity. In most countries, the management company needs a license, or an exemption, in the jurisdiction where it is set up. Most managers set it up in the United States, and that dominance shows up on two different measures. By the number of the largest firms, the United States is home to 48 of the 66 managers running $10 billion or more, about 73%, according to the leading industry rankings. By share of assets, the U.S. lead is real but narrower; the chart below shows where the world’s hedge fund AUM is actually managed.

In the United States, investment advisers are regulated under the Investment Advisers Act of 1940. For decades, most hedge fund managers fell outside it. A long-standing exemption let an adviser with fewer than 15 clients avoid registration, and because each fund counted as a single client, a manager could run several funds and still qualify. After the 2008 crisis, the Dodd-Frank Act of 2010 repealed that exemption and brought most private fund managers within the Act’s reach, either as registered advisers or under one of a few narrower exemptions.

Today, a manager generally does one of two things. It can register as a Registered Investment Adviser (RIA), with the U.S. Securities and Exchange Commission (SEC) or with a state if it is smaller, and take on a full compliance program. Or it can rely on an exemption and file only a short report as an Exempt Reporting Adviser (ERA).

The key dividing line is $150 million in private fund assets under management: below it, a manager that advises only private funds can usually report as an ERA rather than register. Above it, SEC registration is required. A handful of advisers sit outside both boxes, among them foreign private advisers, family offices, and managers who don’t advise on securities at all.

| Criterion | Exempt Reporting Adviser (ERA) | Registered Investment Adviser (RIA) |

|---|---|---|

| AUM / scope | §203(m) < $150M private-fund AUM; §203(l) VC funds only, no AUM cap | A manager advising only private funds: registration required at $150M. Any other manager: SEC-eligible from $100M, mandatory at $110M; below $100M, register with the state |

| Compliance program | Not required | Required: written policies, a Chief Compliance Officer (CCO), annual review |

| Code of ethics | Not required | Required: personal-trading reports, pre-clearance |

| Custody rule | Not required | Required: qualified custodian; GAAP audit to LPs within 120 days |

| Marketing rule | Not directly applicable | Required: performance substantiation, testimonial limits |

| Form PF* | Not required | Required for registered private-fund advisers (≥ $150M, annual); large hedge fund advisers (≥ $1.5B) file quarterly |

| SEC examination | Possible but rare | Regular examination cycle |

So almost every U.S. hedge fund manager ends up in one of these two tiers: an ERA while it is small or VC-only, and a full RIA once it crosses $150 million. Registration adds a CCO, a written compliance program, custody, a marketing review, Form PF, and SEC examinations, and often $150,000 to $300,000 a year in cost. These two tiers are not the whole map, though. A manager whose fund trades futures or swaps may also have to register with the Commodity Futures Trading Commission (CFTC) and the National Futures Association (NFA) as a commodity pool operator, and smaller or non-U.S. managers can fit other narrow exemptions.

The management company usually sits close to home, where the principals are based and where the capital comes from. The fund entities are a different story: they are often more varied and can sit across several jurisdictions, chosen to fit the investors and the assets.

Regulating the fund vehicle

The previous section was about regulating the manager. A separate question is whether the fund vehicle itself is regulated as a product, and the answer depends on where the fund is set up, not on where the manager sits.

In the United States, the weight of hedge fund regulation falls on the manager, not the fund. A pooled fund would ordinarily be an “investment company” under the Investment Company Act of 1940 and have to register, but hedge funds are built to fall outside that Act by relying on one of two exclusions:

Fit one of these and the fund is not registered or supervised as a product. There is no U.S. fund regulator licensing the vehicle; what applies instead is the manager’s regulation, set out above, and the rules on offering interests, set out below. One practical footnote: a §3(c)(7) fund still keeps its holders below 2,000 to avoid triggering reporting under the Securities Exchange Act.

Offshore, the picture flips. Once a vehicle is set up in a center such as the Cayman Islands or the British Virgin Islands (BVI), that vehicle is regulated as a fund in its home jurisdiction. It must register with or be recognized by the local regulator, appoint local service providers such as an administrator, auditor, and custodian, and meet economic-substance requirements. That adds a recurring layer of registration and administration cost. It is the price of going offshore, and for a fund raising non-U.S. or U.S. tax-exempt capital it is usually one worth paying.

So the domicile choice is a real decision, made at the level of the fund vehicle and independently of where the manager is regulated. Five offshore centers host most funds, each offering a ladder of fund types from lightly regulated private vehicles to fully authorized retail funds. The Cayman Islands list is below; switch tabs for BVI, Gibraltar, Jersey, and Guernsey.

| Fund type | License / registration | Investors | Notes |

|---|---|---|---|

| Licensed fund | Mutual fund license required | Retail, no restrictions | ~0.3% of CIMA mutual funds (40 of 13,008). Registered office, administrator, CIMA fit-and-proper showing. |

| Administered fund | None, if the administrator holds a CIMA license & provides the principal office | Retail, no restrictions | ~1.9% of CIMA mutual funds. Must appoint a Cayman Mutual Fund Administrator. |

| Registered fund | Exempt if each investor subscribes ≥ $100,000, or shares list on a recognized CIMA exchange | Professional / accredited, min. $100,000 | ~68.9% of CIMA mutual funds, the dominant category. |

| Limited investor (“exempt”) fund | Registration required | ≤ 15 investors; may appoint/remove the operator by majority | — |

| Private fund | Register with CIMA within 21 days of accepting commitments; single-investor exempt | Closed-end; no statutory minimum | 17,910 private funds at Q1 2026. Requires audited accounts from a CIMA-approved auditor, plus valuation and safekeeping functions, though the custodian role can be disapplied. |

| Fund type | License / registration | Investors | Notes |

|---|---|---|---|

| Private Fund | AIFM registers / licenses under AIFMD (by AUM) | Up to 50 investors in an identifiable group | Financial Services Act 2019. Largely unregulated beyond AIFMD if marketed into the EEA. No custodian or IM required. |

| Experienced Investor Fund (EIF) | FS Regulations 2020 (as amended 2022): legal opinion within 10 days, or 10-day pre-notice | Net worth over €1M (excluding home and pension), or professionals | Companies: ≥ 2 GFSC-approved directors; trusts: 2 trustees; plus an authorized administrator. |

| UCITS, Retail Fund | UCITS license | Ordinary investors | Invests in listed securities; independent depositary required. |

| Non-UCITS Retail Fund | Authorized under the FS Act 2019 | Ordinary investors | Typically not securities, but may get GFSC permission. |

| Protected Cell Company (PCC) | Corporate overlay (Protected Cell Companies Act 2001); each cell an EIF or Private Fund | Depends on the cell | Ring-fences cells like the Cayman SPC / Delaware Series LLC. Popular for parallel strategies & crypto. |

| Fund type | License / registration | Investors | Notes |

|---|---|---|---|

| Professional fund | FSC recognition required | Professional investors, min. $100,000 | ~39% of recognized funds (859 of 2,221), still the most popular. Full set: IM, administrator, auditor, custodian. |

| Private fund | FSC recognition | ≤ 50 investors, or offered on a private basis only | Full set: IM, administrator, auditor, custodian. |

| Public fund | FSC registration (s.45) | No restrictions | Retail offerings; strict FSC oversight (prospectus, ongoing supervision). |

| Private Investment Fund (PIF) | FSC recognition under SIBA; closed-end only | ≤ 50 investors, or private placement, or professional (min. $100,000) | Now the third-largest category (429, ~19%), behind professional funds. Needs an appointed person, an auditor, and a BVI authorized representative. |

| Fund type | License / registration | Investors | Notes |

|---|---|---|---|

| Jersey Private Fund (JPF) | Consent under the Collective Investment Funds (Jersey Private Funds) Order 2025 (via CoBO) | No cap (restricted-group test); each “professional” / “eligible” and/or ≥ £250,000 | Requires a regulated Designated Service Provider in Jersey. No director / trustee / GP / resident auditor required. |

| Expert Fund | Administrator certifies compliance with the Expert Fund Guide | “Expert Investors”, institutions, professionals, or ≥ $100,000 | Popular regulated vehicle. Two experienced resident directors, administrator, auditor. |

| Unregulated Eligible Investor Fund | Outside the CIF Law (Order 2008) | Eligible investors, min. $1M | No resident directors / administrator / custodian. A registered office in Jersey suffices. |

| Eligible Investor Fund | JFSC authorization under the CIF Law 1988 | “Eligible Investors”, min. $1M | Two experienced resident directors, administrator / manager, asset safe-keeping. |

| Unclassified CIF | JFSC authorization under the CIFL | No restrictions; minimum case-by-case | Trustee Jersey-located, capital ≥ £250,000; manager Jersey-registered. Residual catch-all. |

| Listed Fund | Administrator certifies (Listed Fund Guide), Three-day turnaround | Ordinary investors | Closed-end, listed on a recognized exchange. ≥ 2 resident directors, administrator, auditor. |

| Fund type | License / registration | Investors | Notes |

|---|---|---|---|

| Registered CIS | Register with GFSC; administrator + custodian (open fund) | Ordinary investors | Registration takes one business day. |

| Private Investment Fund (PIF) | Register under PIF Rules 2025; administrator required (GP license if Guernsey GP) | No cap; QPIF for Qualifying Private Investors; Family PIF for a family relationship | QPIF + Family PIF. Not required to be audited unless the documents require. One-business-day turnaround. |

| Manager-led product | Register with GFSC; AIFMD; administrator + custodian | Ordinary investors | Needs one Guernsey-regulated IM. The one fund type carrying an AUM marker: “over EUR 100M.” |

| Authorized, Class B | Fund registration; administrator + custodian | Only qualified investors | — |

| Authorized, Class Q | Fund registration with GFSC | Only qualified investors | — |

| Authorized Closed-Ended Fund | Register under the Fund Rules | Only qualified investors | Larger funds; higher regulatory scrutiny. |

We have now covered two of the three layers of regulation: the manager and the fund itself. The third and final layer is the offering: how, and from whom, a fund may raise capital.

Offering to investors

Bringing an investor into the fund means selling them an interest in it, and that interest is a security. Selling securities is its own regulated activity: almost every country sets rules on who may be offered, how, and with what disclosure.

In the United States, any sale of securities must be registered with the SEC or fit an exemption. Most hedge funds rely on Regulation D, the safe harbor adopted in 1982, which lays out three paths: Rule 504, Rule 506(b) and Rule 506(c). Rule 506(b) is the one most funds use.

| Dimension | Rule 504 | Rule 506(b) | Rule 506(c) |

|---|---|---|---|

| Max. amount | $10M in any 12 months | No limit | No limit |

| Investors | No quantity limit; need not be accredited | Unlimited accredited plus up to 35 sophisticated non-accredited | Unlimited accredited, no non-accredited; “reasonable steps” to verify status |

| Documentation | Material disclosures may be required | Non-accredited get mandatory disclosures; a private placement memorandum (PPM) is usual | PPM optional; material-facts duty remains, so usually prepared |

| General solicitation | Prohibited, some exceptions | Forbidden, no exceptions | Allowed |

| SEC notification | Form D within 15 days of first sale | Form D within 15 days | Form D within 15 days |

| Resale | “Restricted,” some exceptions | “Restricted”; 1-year bar on third-party disposition | “Restricted”; 1-year bar |

In practice, almost every hedge fund offers under Rule 506 and sells only to accredited investors, so the real threshold question is who counts as accredited.

≥ $200K / $300K

- On your own, or with a spouse or partner

- In each of the last two years

≥ $1M net worth

- Excluding your primary residence

- Or an entity with ≥ $5M in assets

License or insider

- A Series 7, 65 or 82 in good standing

- A knowledgeable employee of the fund

Source: Securities Act of 1933, Rule 501(a) (Regulation D).

The rules so far cover offers to U.S. investors. Most funds raise from abroad as well, and that side carries two separate questions: how the United States treats an offshore sale, and what the law of the investor’s own country requires.

- An offshore transaction; the buyer is outside the United States

- No directed selling efforts inside the United States

- National private placement regime (NPPR): register country by country to market actively

- Or reverse solicitation: the investor approaches you

On the U.S. side, the safe harbor is Regulation S. It places offers and sales made outside the United States beyond the reach of the Securities Act’s registration requirements. Two conditions carry it: the sale must be an offshore transaction, meaning no offer is made to a person in the United States and the buyer is outside the United States when it commits, and there must be no directed selling efforts inside the United States, meaning no marketing that conditions the U.S. market. Most funds run Regulation S alongside Regulation D, the onshore vehicle selling to U.S. accredited investors under Rule 506 and the offshore vehicle selling to non-U.S. investors under Regulation S. Interests sold under Regulation S stay restricted, with a compliance period before they can flow back to U.S. persons.

Regulation S only answers the U.S. question. It does not let a fund market wherever it likes. A fund interest is a security, and most developed countries regulate the offer of one under their own private-placement and fund-marketing rules. A fund that takes foreign capital has to clear the law of each jurisdiction where it actually offers, not U.S. law alone.

Europe is the clearest case. Marketing a fund to investors in the EU is governed by the Alternative Investment Fund Managers Directive (AIFMD). A non-EU fund cannot simply approach EU investors: to market actively it must register country by country under each member state’s national private placement regime, meet that regime’s transparency and reporting conditions, and even then usually reach only professional investors, not the retail public.

The usual way around that is reverse solicitation. Where an EU investor approaches the fund on its own initiative, with no prior solicitation from the manager, the contact is not treated as marketing, and neither the AIFMD nor the parallel MiFID II rules on cross-border services apply. It is a narrow, fact-sensitive route: the investor, not the manager, must start the conversation, regulators read it strictly, and the EU’s newer pre-marketing rules have tightened what qualifies. Many offshore funds take European capital this way, but only where the approach is genuinely investor-led, never as a cover for active selling.

Source: Securities Act of 1933, Regulation S (Rules 901–905); AIFM Directive 2011/61/EU; MiFID II.

The fund’s legal documents

The structure section shows the parties and the agreements that tie them together. Here are those agreements as actual documents: the core paperwork behind almost any fund, what each one is, and why it has to exist. A registered manager carries a few more than an exempt one, but the spine is the same.

ConstitutionalLimited Partnership Agreement / Operating Agreement

The fund’s governing document, and the one that matters most. It sets the deal between the manager and the investors: the management and performance fees, how profits and losses are allocated, voting and governance, transfer and withdrawal rights, lock-ups and gates, indemnification, and how the fund winds up. A limited partnership uses an LPA; an LLC uses an Operating Agreement, which does the same job.

OfferingPrivate Placement Memorandum (PPM)

The disclosure document handed to investors before they subscribe. It describes the strategy, the terms, the fees, the conflicts of interest, and, above all, the risk factors. The PPM is the manager’s main shield against a fraud claim: it puts every material fact on the table so an investor cannot later say it wasn’t told.

AdmissionSubscription Agreement and Investor Questionnaire

The contract by which an investor commits capital and is admitted to the fund. The investor confirms it has read the PPM and that it clears the eligibility gates: accredited investor, qualified purchaser, or qualified client (the net-worth or AUM test that lets a manager charge a performance fee). It also answers an AML/KYC questionnaire on its identity and source of funds. This is where the manager builds its record that every investor was allowed in.

ManagementInvestment Management Agreement (IMA)

The contract between the fund and the management company. It appoints the manager, sets the scope of its discretion over the portfolio, fixes the management fee, and states its standard of care and indemnification. It is what makes the manager’s authority and fee legally enforceable against the fund.

The entitiesGP and Management Company Operating Agreements

The internal governing documents of the manager’s own entities, the general partner and the management company. They set who owns those entities, how the carried interest and the management fee are split among the principals, and who controls decisions. The structure section explains why the GP and the manager are often two separate entities; these are the documents that run each one.

Investor-specificSide Letters

Bilateral agreements with individual investors, usually large or early ones, that vary the standard terms: fee discounts, capacity or co-investment rights, extra reporting, and most-favored-nation clauses that promise no one else gets a better deal. They let a manager accommodate a key investor without reopening the fund documents for everyone.

ComplianceCompliance Manual and Code of Ethics

The manager’s internal rulebook. A registered adviser must keep written policies and procedures and name a Chief Compliance Officer under Rule 206(4)-7, plus a code of ethics governing staff personal trading and the handling of material non-public information (MNPI) under Rule 204A-1. An exempt manager still keeps baseline anti-fraud and MNPI policies.

ComplianceAML/KYC Policy

Anti-money-laundering (AML) and know-your-customer (KYC) procedures for screening investors and verifying their source of funds, usually overseen by a Money Laundering Reporting Officer. Expected of onshore funds and a hard requirement in offshore domiciles, where the regulator will ask to see it.

Regulatory filingsForm ADV and Form D

The two filings that put the manager and the offering on the regulatory record. Form ADV registers the adviser with the SEC or a state, in full for an RIA or a short version for an ERA. Form D is the notice claiming the Regulation D private-offering exemption, filed within 15 days of the first sale. Both come up in the regulation and offering sections.

Service providersService Provider Agreements

The engagement contracts with the fund’s outside providers: the administrator, the prime broker, the custodian, and the auditor. They allocate duties, fees, liability and confidentiality, and offshore regulators often require some of these providers to be appointed before the fund can take money.

A crypto fund adds a layer on top of this set: a digital-asset custody agreement, SAFT (simple agreement for future tokens) or token side letters, and extra PPM risk disclosures covering smart-contract, fork, slashing, oracle, and bridge risk.

Fees and economics

A hedge fund manager makes its money from two fees: a management fee charged on the fund’s assets, and a performance fee charged on its profits.

The management fee covers the cost of running the firm: its people, premises, technology, and compliance. It is charged as a percentage of assets under management and paid throughout the year, whether the fund gains or loses. It sustains the business rather than enriching the manager.

The performance fee is the manager’s real upside: a share of the profits the fund earns, paid only on gains. It is also known as the carry, or carried interest. The name is far older than hedge funds: it is usually traced to medieval Genoese and Venetian merchants, and later ships’ captains, who took a fixed share, traditionally about a fifth, of the profit on the cargo they carried. A modern manager’s share of the profits is the direct descendant of that practice and still carries its name.

For decades, the convention was “two and twenty”: a 2% management fee and a 20% performance fee. It remains the reference point, but the industry has drifted below it. Most funds now charge less on both, and the averages have edged down year after year. The charts show where managers now cluster and how the averages are trending.

| Average fee | 2018 | 2022 | 2024 | Trend |

|---|---|---|---|---|

| Management fee, % | 1.40 | 1.40 | 1.37 | |

| Performance fee, % | 17.08 | 16.27 | 16.36 |

Fee compression is the norm, not an absolute. A fund that delivers exceptional returns can still command exceptional fees, and one sits far above the rest.

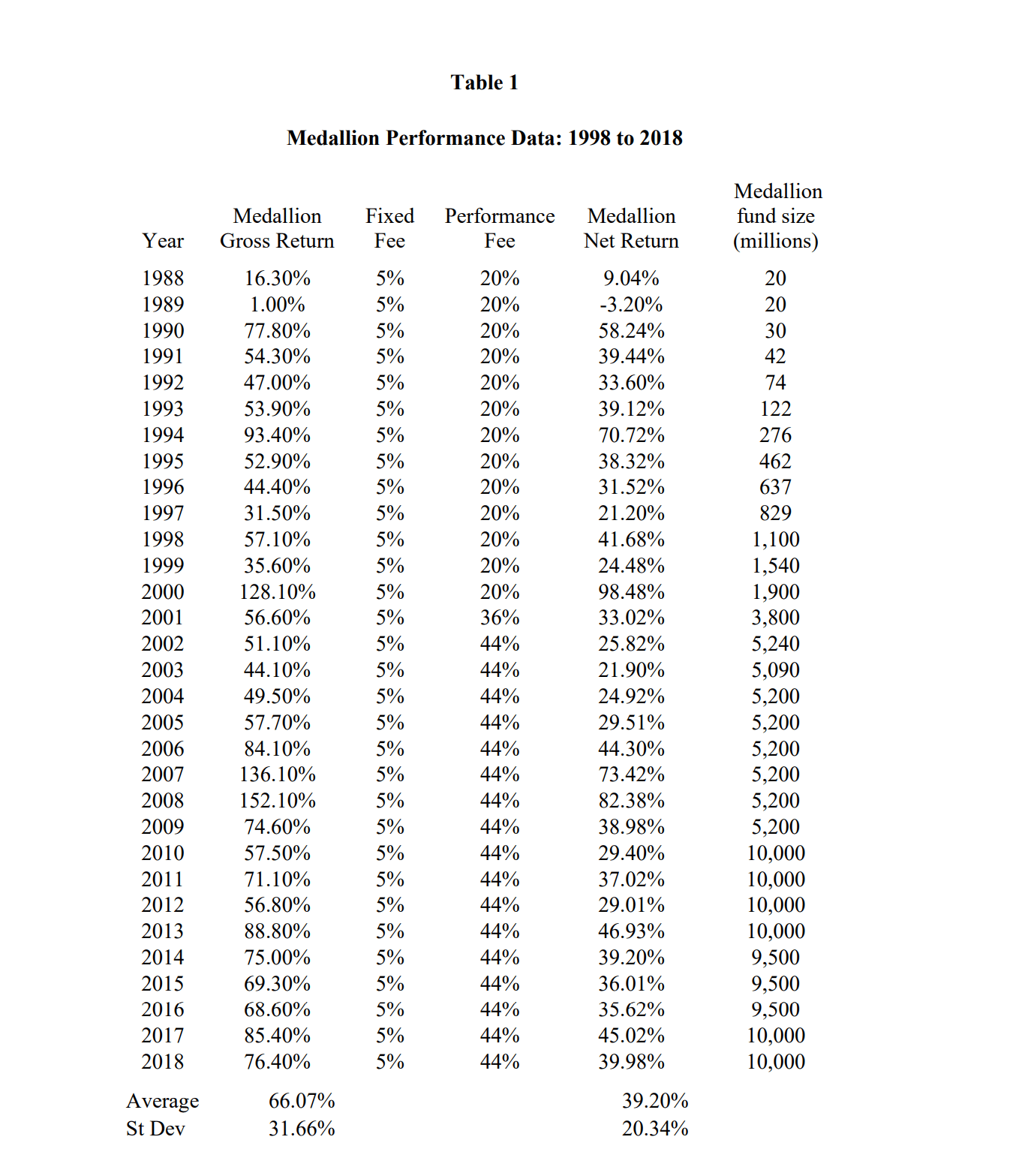

OutlierThe Medallion Fund: 5 and 44

Renaissance Technologies’ Medallion Fund is the standing exception to two and twenty. It charges a 5% management fee and a performance fee that rose over the years from 20% to 44%, well over double the norm. The returns justify it: from 1988 to 2018, the fund averaged about 66% a year before fees and about 39% after them. Medallion has long been closed to outside investors and runs only for Renaissance’s own employees, which helps explain how it sustains such terms. Superior performance commands superior fees.

Two mechanics decide how much of a strong year the manager actually keeps, and both are built to protect investors.

The high-water mark means the performance fee is charged only on new profits. It is the highest value an investment has previously reached; the manager is paid only on gains above it. Consider an investment of $100 that falls to $80 and then recovers to $120. The fee applies to the $20 above the $100 mark, not to the full $40 recovery, so the investor does not pay twice for the same gains.

The hurdle rate is a minimum return the fund must clear before the manager shares in the profit at all; below it, all profit accrues to investors. Funds differ on how the hurdle is measured. Under the gross approach, the performance fee applies to the return above the hurdle before the management fee, so a 12% gross year over an 8% hurdle leaves four percentage points to charge on. Under the net approach, the management fee comes out first: a 12% gross year less a 2% management fee is a 10% net return, so only two points sit above the hurdle. The net approach is the more common, and the more favorable to investors. Only about a quarter of hedge funds use a hurdle at all.

The calculator below shows how a single year’s return is divided between investors and the manager. Adjust the fund’s terms and the annual gross return to see how the split responds, the hurdle included.

This calculator uses the net approach: the performance fee is taken on the gain above the hurdle after the management fee is deducted, the more common of the two conventions described above.

Key deal terms

A cluster of defined terms governs how investors enter, how the performance fee is struck, and how and when money can leave. The 20 most common are grouped below by what they govern, with the typical market figure noted where there is one.

EntryAnchor Investor

The first one or two investors to commit real size, usually at launch when there is no track record yet. In return they tend to get a fee discount, a capacity right, or a place in a founders class. Their commitment is what lets the manager show everyone else that the fund is real.

Share classFounders Class

A share class for early backers that charges less in exchange for coming in before the fund is proven. A common break is around 1 and 10 in place of the standard 2 and 20, often limited to the first $100 million raised or the first year of trading.

EntryMinimum Investment

The smallest commitment the fund will take. Around $1 million is typical, with a range from $100,000 to $5 million, and it is usually lower for a founders class. A higher minimum also helps keep the headcount under the 100-investor limit of a §3(c)(1) fund.

Investor-specificSide Letter

A private agreement with a single investor that changes the standard terms just for them: a fee break, extra reporting, a capacity right, or a most-favored-nation clause. It lets the manager say yes to a key investor without reopening the fund documents for everyone.

Investor-specificMost-Favored-Nation (MFN)

A side-letter promise that if the manager later grants another investor better terms, this investor may take them too. It is normally limited to investors of the same size or smaller, and the manager circulates the menu of side-letter terms once a year so MFN holders can elect.

FeeManagement Fee

A flat annual charge on assets, taken whether the fund gains or loses, to cover salaries and the cost of running the firm. The classic figure is 2%, though 1% to 1.75% is now common, accrued monthly and drawn monthly or quarterly.

FeePerformance Fee (Incentive Allocation)

The manager’s cut of the profits, the “20” in “2 and 20”. The classic figure is 20%, with a range of 10% to 30%. In a partnership it is usually structured as an “incentive allocation” rather than a fee, which is more tax-efficient for the manager.

Performance feeHigh-Water Mark

The highest NAV an investor’s holding has reached before. The performance fee is charged only on gains above it, so the manager is not paid twice for making back the same losses. Enter at $100, fall to $80, climb to $120, and the 20% is taken on the $20 above $100, not the full $40.

Performance feeHurdle Rate

A minimum return the fund must beat before any performance fee is due, often 5% to 8% or a benchmark such as SOFR. A “soft” hurdle then lets the manager charge on all the profit; a “hard” hurdle charges only on the return above the hurdle. Only about a quarter of hedge funds use one.

Performance feeCrystallization

The point at which the performance fee stops being a paper accrual and is actually locked in and taken, usually once a year on December 31 and on any interim redemption for the units that leave. The more often a fee crystallizes, the better for the manager.

LiquidityLock-Up

A period after investing when an investor cannot redeem at all, most often one year. A “hard” lock-up bars withdrawal outright; a “soft” lock-up allows it but charges a fee, commonly 2% to 5%, paid to the fund.

LiquidityRedemption

How an investor takes money out, set by frequency and notice. A common pattern is quarterly dealing on 60 to 90 days’ written notice, though monthly and annual dealing both exist. The fund may also hold back 5% to 10% until the year-end audit confirms the NAV.

LiquidityGate

A cap on how much can be redeemed in any one period, so a rush for the exit cannot force a fire-sale of the portfolio. A fund-level gate is often around 15% to 25% of NAV; an investor-level gate limits each holder instead. Requests above the gate roll into the next period.

LiquiditySide Pocket

A separate compartment inside the fund for illiquid or hard-to-value positions. Investors keep their share but cannot redeem it until the position is sold or marked, which stops people cashing out at a guessed price and leaving the illiquid risk behind.

LiquidityRedemption Fee

A charge for leaving early, typically during a soft lock-up, of around 2% to 5% of the amount withdrawn. It is usually paid to the fund rather than the manager, to compensate the investors who stay for the cost of the exit.

LiquiditySuspension

The manager’s right to halt redemptions, and sometimes NAV calculation, in extraordinary conditions such as markets freezing or pricing becoming impossible. A blunt last resort that was used widely in 2008, and a clause investors read closely before committing.

ProtectionKey Person Provision

A clause that triggers when a named principal, the person the investors actually backed, stops running the fund. It usually lets investors redeem without penalty and freezes new investment until the seat is filled. It is the first protection an institutional investor looks for.

CapitalSeed Investor

An investor who puts up large “day-one” capital in return for a share of the management company’s own economics, often 15% to 25% of its revenue, plus better fees and capacity, usually for a fixed number of years. Unlike an anchor, a seeder buys into the business, not just the fund.

AccountingEqualization

An accounting method that makes every investor pay the right performance fee whatever date they joined, given that the fund runs on one shared NAV. It stops a newcomer being charged for gains it never had, or riding free on the high-water mark built up by others. Common methods are the series-of-shares and equalization-factor approaches.

ComplianceNew Issues

U.S. rules from the Financial Industry Regulatory Authority (FINRA), Rules 5130 and 5131, that limit who can profit from hot IPO allocations. Brokers, fund insiders and certain others count as “restricted persons” and must be carved out of those gains, which is why subscription documents ask whether an investor is one.

Service providers

Every fund works with a handful of outside service providers and signs a separate agreement with each of them.

Reviewing those agreements is a real part of the legal work of launching a fund. The templates almost always come from the provider and are drafted to suit the provider, so each one repays a careful read before it is signed.

Executes, clears, and holds the fund’s trades, lends cash and securities for leverage, and reports the positions used to strike the NAV.

- Financing and margin: lock the rate, the borrowing line and the margin requirement for a fixed period, so the broker cannot reprice or raise margin at will.

- Rehypothecation: cap how far the broker may reuse the fund’s assets. The U.S. 140% limit does not apply offshore.

- Termination and default: notice before any termination without cause, cure periods, and no subjective triggers such as “material adverse change.”

- Broker failure: notice and good-faith pricing before any forced sale, and the broker’s own insolvency as an event of default.

Keeps the books, calculates the NAV, runs investor onboarding and AML/KYC checks, and processes subscriptions and redemptions.

- Standard of care: liability only for gross negligence, willful misconduct or fraud, not for ordinary mistakes.

- Liability cap and indemnity: the cap is often a multiple of annual fees; narrow the broad indemnity the administrator asks of the fund, and carve out its own gross negligence.

- NAV and pricing: who is responsible for valuations and pricing sources, plus a clear NAV-error policy fixing the threshold and who pays to correct mistakes.

- Fees and exit: the fee basis and minimums, and a workable notice period to change administrator.

Holds the fund’s assets, kept separate from the manager. For a registered adviser this must be a qualified custodian; for crypto, a digital-asset custodian.

- Liability for the custodian and for any sub-custodian it appoints, including loss of assets.

- Segregation of the fund’s assets, and what happens if the custodian becomes insolvent.

- For crypto: audited control reports, insurance, and how private keys are held.

Audits the annual financial statements and signs the report investors rely on. Independence rules make this the least negotiable of the contracts.

- Liability: auditors cap their exposure, often at a multiple of fees, and exclude indirect losses. The cap level is the main lever.

- Reliance: who may rely on the report, and any release the auditor asks the fund to give.

- Scope, timetable and fees: the audit deadline matters offshore, where accounts are due within a set window.

Introduces investors and helps raise capital, usually for a fee on the money it brings in.

- Fee and tail: the fee, commonly 1.5% to 2.5%, and the tail period, often 12 to 24 months, when the agent still earns on investors it introduced. Keep the tail short and the introduced list defined.

- Exclusivity: its scope, with carve-outs for relationships the fund already has.

- Indemnities: usually reciprocal but not symmetrical. The fund covers offering-document claims; the agent covers its own unauthorized statements.

Sit on the board of an offshore fund vehicle and oversee how it runs. Investors expect them in Cayman and similar structures.

- Fees and capacity: the annual fee, and how many other boards the director already sits on.

- Indemnity and insurance: an indemnity from the fund plus directors-and-officers (D&O) cover, with the usual carve-outs for fraud and gross negligence.

- Removal: the fund’s right to replace a director.

Across all of them the same few levers recur: the standard of care, a cap on liability, the indemnities each side gives, and how and when the agreement can be ended.

Regulatory trends and what to watch

For most of the last decade, the regulatory line moved in one direction: toward tighter oversight of private funds. Over the past two years, it has reversed. The shift has come from two directions at once: the courts and a change of administration in Washington.

In mid-2024, the Supreme Court reset the ground under every federal regulator. In Loper Bright Enterprises v. Raimondo, it ended Chevron deference. A court no longer defers to an agency’s reading of an ambiguous statute and instead interprets it for itself. A day earlier, in SEC v. Jarkesy, it held that the SEC must bring securities-fraud penalty cases in a federal court before a jury, not before its own in-house judges. Together, the two decisions made the SEC’s rules easier to challenge and its enforcement slower to bring.

Hedge fund managers felt the change almost immediately. In June 2024, the Fifth Circuit vacated the SEC’s Private Fund Adviser Rules in full. That 2023 package would have required quarterly investor statements, an annual audit, and limits on preferential side letters; the court held that the agency had no authority to impose them. Five months later, a Texas court struck down the SEC’s expanded dealer rule, which had threatened to pull actively trading funds into broker-dealer registration. Both fell for the same reason: the SEC had exceeded the authority Congress gave it.

The change of administration pushed in the same direction. Paul Atkins became SEC chair in April 2025 on an openly deregulatory program. The Form PF overhaul, which would have demanded far more data from large hedge fund advisers, has been delayed more than once, now to October 2026. The Commission has said it intends to narrow what it collects. Atkins has also signaled an interest in widening retail access to private funds, revisiting the long-standing limits on who may invest.

Even the formation requirements eased. In March 2025, the Financial Crimes Enforcement Network (FinCEN) rewrote the Corporate Transparency Act’s beneficial-ownership rule to cover only foreign entities, dropping the filing entirely for funds and managers formed in the United States.

The near-term direction is more of the same: lighter federal oversight, fewer new filings, and pressure to open private funds to a broader base of investors. Several developments are worth watching: whether the SEC re-proposes any private-fund rules in a narrower form built to survive the new best-reading standard; whether a clearer framework emerges for crypto funds; and whether the accredited-investor and qualified-purchaser thresholds move. The one safe assumption is that the rules will keep moving. Confirm the current position from the primary sources before relying on it.

The two Supreme Court decisions behind the shift

Loper Bright Enterprises v. Raimondo (June 28, 2024). Overruled the 40-year Chevron doctrine. Courts had deferred to any reasonable agency reading of an ambiguous statute; now they decide the best reading themselves, so an agency must show its rule is the law’s best interpretation, not merely a permissible one.

SEC v. Jarkesy (June 27, 2024). When the SEC seeks civil penalties for securities fraud, the Seventh Amendment gives the defendant a right to a jury in a federal court, ending the agency’s use of in-house administrative judges for those cases. For funds, the first makes SEC rules easier to overturn; the second raises the cost and slows the pace of SEC enforcement.

What the vacated Private Fund Adviser Rules would have required

The SEC adopted the rules in August 2023; the Fifth Circuit vacated them in June 2024. They would have imposed five duties on private fund advisers: a quarterly statement of fees, expenses, and performance; an annual audit of each fund; a fairness or valuation opinion on adviser-led secondaries; a bar on certain restricted activities without disclosure or investor consent; and limits on preferential treatment in side letters on redemptions and information unless offered to all. None now applies. Managers are back to the prior baseline: the Advisers Act anti-fraud rules and the terms in their own fund documents.

That brings the guide to a close. We have gone from what a hedge fund is and where the name began, through how one is structured, regulated, documented, offered, and run. The rules will keep shifting, as this last section shows, but the architecture underneath stays much the same. We hope it has been a useful guide to building a hedge fund.

Disclaimer

This guide is for informational purposes only and does not constitute legal advice. Fund structuring, offshore domicile rules, and the U.S. private-offering and adviser-registration regimes change with legislation and regulator practice; the figures, thresholds, and dates here are current as of the points noted and may shift. For advice on a particular fund, please contact Buzko Krasnov directly.